お世話になっております。

バーチャルキャリアアドバイザーのなるはやちゃんです。

なるはやちゃ~ん!

あら、なるほどくん、どうしたの?

給与明細の見方を教えてほしいんです!

給与明細!

確かに、聞きなれない言葉がちょこちょこ書いてあって、

よくわからないですよね~。

では今回は、給与明細の見方について、解説していきたいと思います!

よろしくお願いします!

給料の「締め日・支給日」とは

まずは、給与の「締め日・支給日」について解説します!

締め日・支給日のことは知ってますか?

もちろん知ってますよ〜! でも、念のため解説をお願いします!

はーい!ではまず、給料の締め日についてです。

給料の締め日

これは、勤怠の期間を表すもので、 毎月1日~末日を勤怠の期間としている会社は「末締め」と呼ばれ、 毎月21日~翌月の20日の場合は「20日締め」と呼ばれます。

続いて、支給日についてです!

給料の支給日

これは「給与が支払われる日」のことです。 会社はいつでも好きな日に支給ができるわけではなく、 毎月一定の日を支給日とする必要がありますね。 一般的には25日が支給日、給料日の会社が多いです。

なるほど〜!ありがとうございます!

25日に多いのはどうしてなんですかね?

うーん。会社側の都合で、締めの業務や月末の業務を分ける、といったことと、 公共料金やカードの引き落としなどの、個人の支払い日に配慮しているといった背景があるみたいだね。

なるほど〜!

給与明細全体の構成

続いては、給与明細全体の構成について!

給与明細には、決まったフォーマットというのはありません。

ですが、給与明細の構成に必要なのは、

勤怠・支給・控除・差引合計のこの4つですね。

どの給与明細にも、必ずその4つは書かれてるってことですか?

そうそう!じゃあ1つずつ解説していきます。

勤怠

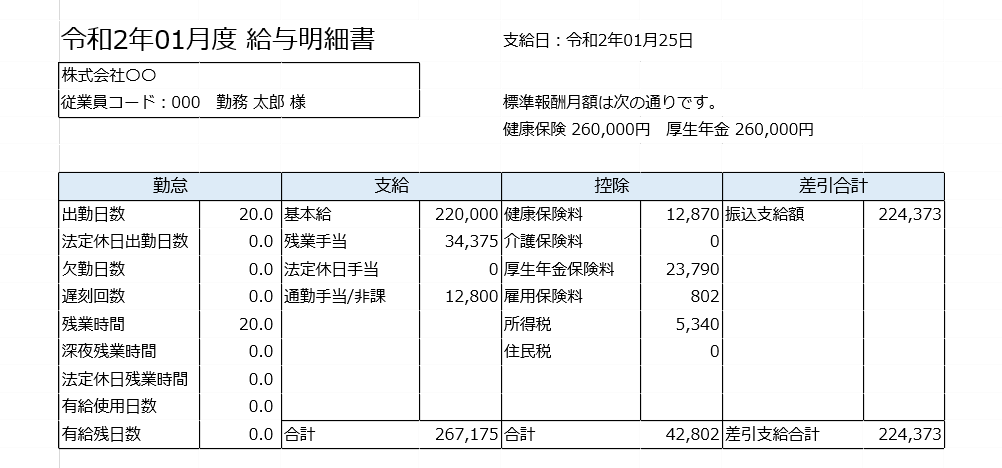

勤怠の欄に表示されるのは、出勤日数・欠勤日数・残業時間・深夜時間・有給利用数などの 実績の時間や日数が表示されます! この実績というのは、先ほどの「締め日」の期間のものですね。

支給

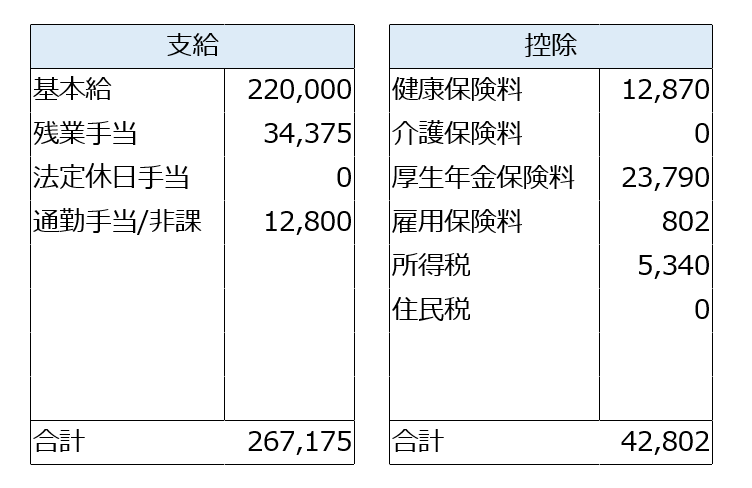

支給というのは、基本給や残業手当などの「プラスになる金額」が記載されます。 もし、欠勤してしまった場合は、支給の欄でマイナスが記載されることもあります。

もらえる金額ってことですね。 残業手当はどんな計算式なんですか?

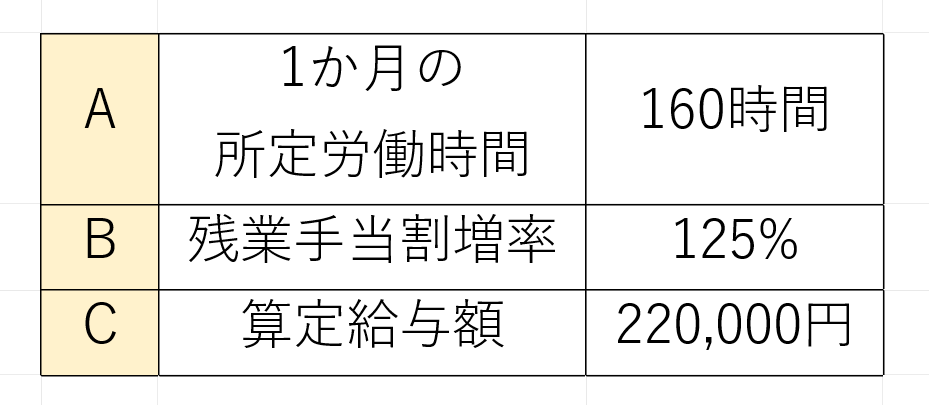

はい。残業手当の計算式は、こちらです!

残業手当の計算式

まずは、算定給与額(C)を1か月の所定労働時間(A)で割り、1時間あたりの単価を出します。 そして、1時間の単価×残業時間×125%(B)を計算した値が、残業手当となります。

この「所定労働時間」と「算定給与額」っていうのは、

会社ごとに違ってくるやつですか?

その通り!会社の就業規則などをよく確認してみてくださいね。

なるほど!了解です!

控除

続いては、「控除」の欄です。 控除、というのは「マイナスされる金額」のことで、 支給した金額から会社が自動的に控除しているものが、この欄に記載されています。

あー「天引き」とか言われてるやつですね。

それそれ!では、こちらも見ていきましょう。

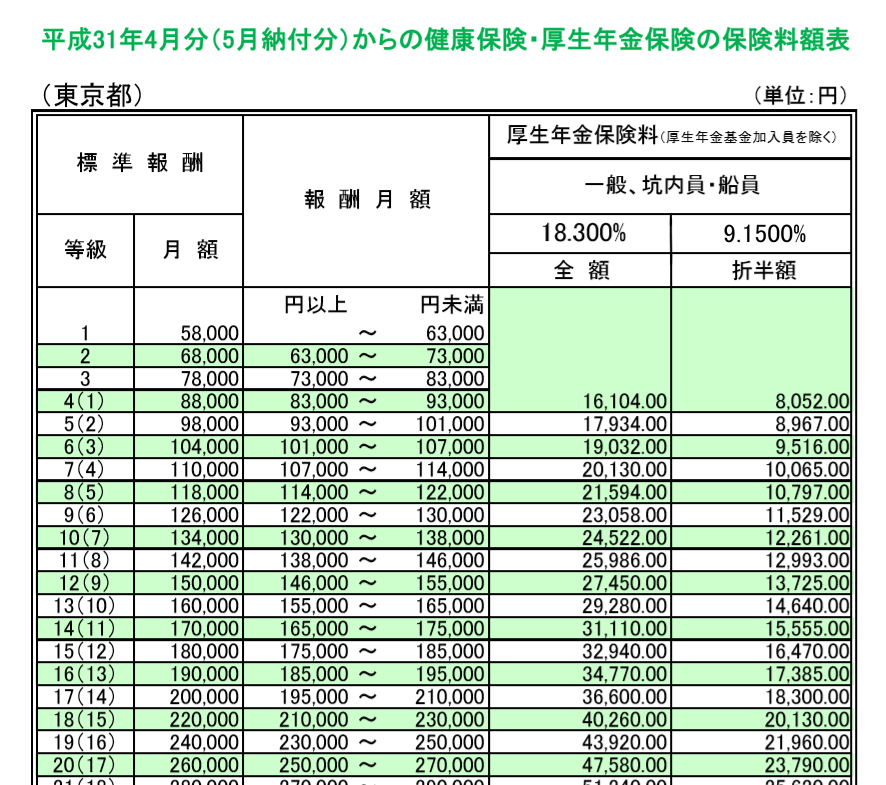

厚生年金保険料の計算方法

厚生年金保険料は、基本給と通勤手当を足した「報酬月額」というものを算出し、 その報酬月額に当てはまるものを、厚生年金保険料額表から見つけ出して計算します。 健康保険料は、報酬月額から割り出した「標準報酬」に9.15%をかけたものとなります。 (東京都で、協会けんぽの場合)

たしか、会社が入っている保険組合によって

保険料は変わってくるんですよね〜

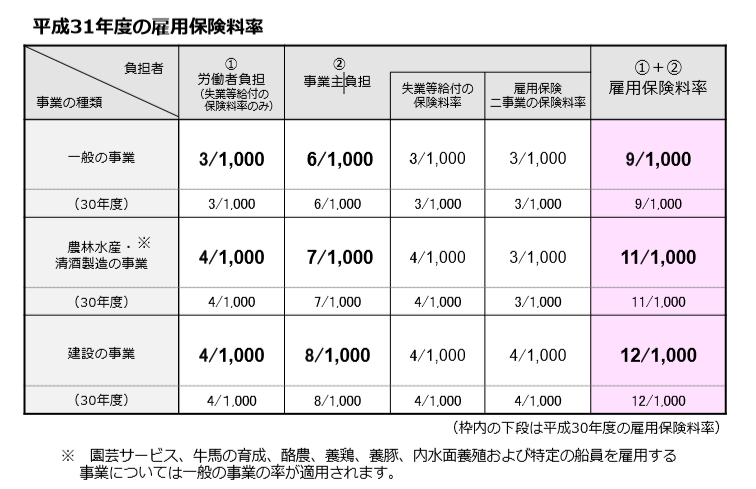

雇用保険料の計算方法

雇用保険料は「労働の対価」として支払われたものと、通勤手当を足したものに対して、 雇用保険料率をかけた金額となります。

「労働の対価」というのは具体的には何のことですか?

基本給や残業手当などがそれにあたりますね。

慶弔見舞金や経費精算などは「労働の対価」には含まれず、算出対象にはなりません。 計算方法は、基本給と残業手当と通勤手当を足したものに、雇用保険料率の1000分の3をかけます。

ちなみに、雇用保険料率というのは、どこでわかるんですか?

厚生労働省のHPで確認できます!

なるほど〜!

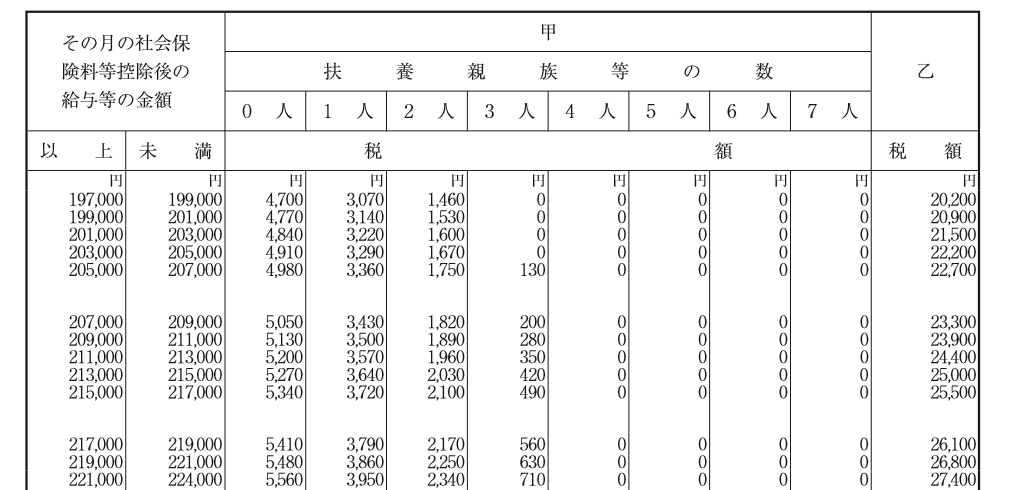

所得税の計算方法

所得税は、課税対象の基本給や手当の合計から、社会保険料と雇用保険料を引いて、 残った金額を、源泉徴収税額表にあてはめます。

結構、表にあてはめることが多いんですね。

そうですね〜

この場合は、基本給、残業手当を足したものをAとし、 健康保険料、厚生年金保険料、雇用保険料を足したものをBとします。 そして、そのAからBを引いた額を、下記の「源泉徴収税額表」にあてはめます。 この方は扶養家族が0人なので、所得税は5340円ですね。

なるほど!

差引合計

最後に、給与明細の「差引合計」の欄を解説します。

これがいわゆる「手取り」ってやつですかね?

その通り!

先ほどの「支給」の合計から、「控除」の合計が引かれたものが、

差引支給合計となり、 この金額が指定した金融機関の口座に振り込まれます。

やったぜ!

給与の計算は会社がしてくれるので、無関心の方も多いのではないでしょうか?

この機会に、自分の支給額と控除額について調べてみるのもいいかもしれませんね!

おわりに

以上、給与明細の見方についてご紹介しました〜!

・決まったフォーマットはない

・大きく勤怠、支給、控除、差引合計の4つで構成されている

という感じです!

なるほどくん理解できた?

ありがとうございます!

給与明細、完全に理解しました!

給与アップを目指したい、自分に合った仕事を見つけたい!と思ったら、

LINEで手軽に転職活動を始められる

「なるはやキャリア相談室」にご相談ください!

LINEで転職活動!

なるほど、お手軽ですね!